Key Points

- China increased export controls on critical materials where it has a dominant share of production, two weeks ahead of a scheduled face-to-face meeting between leader Xi Jinping and President Trump.

- The US President has threatened retaliation, including 100% tariffs on Chinese imports.

- The S&P 500 plunged on Friday, and gold recovered above $4,000 per ounce as investors fear an escalating trade war.

In an escalation of the ongoing trade war between the US and China, China expanded export controls over a range of critical materials just two weeks ahead of a face-to-face meeting scheduled between Chinese leader Xi Jinping and President Trump, at APEC, in South Korea.

BEIJING, Oct 9 (Reuters) – China dramatically expanded its rare earths export controls on Thursday, adding five new elements and extra scrutiny for semiconductor users as Beijing tightens control over the sector ahead of talks between Presidents Donald Trump and Xi Jinping. The world’s largest rare earths producer also added dozens of pieces of refining technology to its control list and announced rules that will require compliance from foreign rare earth producers who use Chinese materials.

In a Truth social post, President Trump said the Chinese move was a “real surprise” and questioned whether the scheduled meeting should proceed.

NEW YORK, Oct 10 (Reuters) – Stocks fell sharply on Friday, with the S&P 500 and Nasdaq suffering their biggest one-day percentage declines since April 10, while Treasury yields dropped and the U.S. dollar weakened as comments by President Donald Trump reignited worries over a U.S.-China trade war. After markets closed on Friday, Trump said he was raising tariffs on Chinese exports to the U.S. to 100% and imposing export controls on “any and all critical software” in a reprisal against recently announced export limits by China on rare earth minerals critical to tech and other manufacturing.

Stocks

The S&P 500 plunged through short-term support at 6700 on fears of an escalating trade war. A follow-through below 6500 would offer a target of 6350 for the correction.

Financial Markets

Financial market conditions support high stock prices, with the Chicago Fed NFCI Index declining to -0.546 on October 3.

Bitcoin — our canary in the coal mine — retreated sharply to test support at 110K. Follow-through below 108K would warn of a significant contraction in financial market liquidity.

Treasury Markets

10-year Treasury yields are headed for another test of long-term support at 4.0%, shown on the weekly chart below.

Bond market guru Jim Bianco maintains that, with inflation “sticky” at 3.0%, a healthy yield curve would require the Fed to keep short-term rates 100 basis points higher at 4.0%, leaving little room for further cuts. He also warns that the 10-year should be another 100 basis points higher, at 5.0%.

The current trade war escalation will likely ensure the Fed cuts below 4.0%, raising the specter of a steep rise in inflation.

Consumers

The University of Michigan survey reports declining consumer sentiment in October, reaching lows not seen since the pandemic.

Perceptions of current economic conditions are lower than when President Biden left office, leaving the GOP House majority at risk in the 2026 midterms.

Consumer expectations have plunged to similar lows.

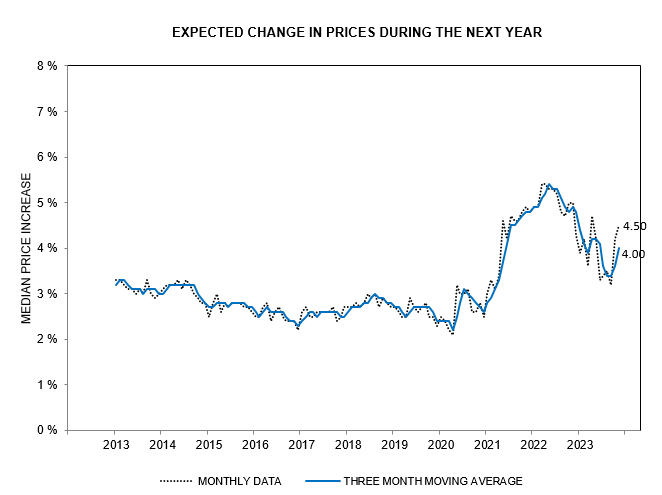

Expected price increases have moderated in recent months, but remain high at 4.6% p.a.

Long-term expectations, likewise, are a high 3.7%, well above the Fed’s 2.0% target.

Dollar & Gold

The US Dollar Index continues to test long-term support at 98, as shown in the weekly chart below. A breach would confirm our long-term target of 90.

Gold retraced to test its new support level after reaching our target of $4,000 per ounce almost three months ahead of schedule. Escalating trade tensions with China sparked another rally, and follow-through above recent highs would signal a fresh advance, with a target of $4,250.

Silver is more volatile, and tall shadows at $50 per ounce signal profit-taking and increase the likelihood of a correction.

Energy

Nymex WTI Light Crude broke support at $60 per barrel in response to trade war fears.

Crude prices below $60 per barrel squeeze shale producers’ margins and threaten US crude production as unproductive wells are closed. The Baker Hughes US oil rig count slipped to 418 from 422 last week.

Base Metals

The Dow Jones Industrial Metals index ($BIM) fell sharply on the weekly chart below, warning of a correction in copper, aluminum, and other base metals, anticipating a fall in demand as the US-China trade war escalates.

Conclusion

Escalating geopolitical and trade tensions threaten to destabilize an already fragile global economy, with precarious fiscal debt levels and stubborn inflation. We anticipate low growth and high inflation and maintain our overweight position in gold and defensive stocks. We are underweight high-multiple technology stocks and avoid exposure to long-term bonds.

The US and China are caught in what is now known as a Thucydides trap. Ancient Greek historian Thucydides recorded the collision of an established hegemon, Athens, and a rising challenger, Sparta, and concluded that war was inevitable. Nowadays, with nuclear-armed adversaries, war seems unlikely. Instead, we will likely see a trade war with the two flexing their economic muscle to secure a dominant position in the global economic order. The US still has a strong military advantage, but China enjoys a similar advantage in industrial capacity. China presently has the upper hand because its leadership is more strategic, while President Trump is more transactional. However, the eventual outcome is uncertain, and we recommend a strong defensive posture to weather the fallout.

We expect increased fiscal spending, suppression of interest rates, and high inflation as the inevitable consequences of war.

The rise of gold and decline of US Treasuries as the global reserve asset will likely continue as tensions escalate in the decades ahead.

Acknowledgments

- CoinDesk: Bitcoin

- Federal Reserve of St Louis: FRED Data

- University of Michigan: Consumer Surveys

- Reuters: Stocks, dollar tumble; Trump says he will raise China tariffs to 100%

- Luke Gromen, FFTT: October 10, 2025

- Jim Bianco & Jeremy Schwartz: AI, Inflation, and the Fed’s Blind Spot

- Baker Hughes: US Oil Rig Count

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He founded PVT Capital (AFSL number 546090), which provides income and growth strategies to wholesale clients.

Colin also co-founded Incredible Charts and writes the popular Patient Investor newsletter.

Using a top-down approach, Colin identifies macro trends in the global economy and then combines fundamental and technical analysis to evaluate opportunities in sectors that stand to benefit.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.