Key Points

- The US economy added 50,000 jobs in December, but employment in cyclical sectors is contracting, indicating a slowing economy.

- Declining cyclical indicators for housing, manufacturing, and transportation, and a declining Coincident Economic Activity Index, also warn of an economic slowdown.

- Average hourly earnings are growing at an annual rate of nearly 4.0%, above the federal funds target range of 3.5% to 3.75%, suggesting that the Fed expects an economic contraction.

- Small-caps are outperforming mega-cap technology stocks, which is typical of the final stage of a bull market.

According to the Bureau of Labor Statistics, the US economy added 50,000 jobs in December, the eighth consecutive month of dismal nonfarm payroll growth.

Excluding government layoffs makes little difference to poor job growth. Private-sector jobs excluding healthcare grew by only 15,900 in December.

Cyclical sectors — manufacturing, construction, transportation, and warehousing — account for 17% of total nonfarm employment in the US but are typically responsible for most job losses during a recession. The sectors have shed 164,000 jobs since their February 2025 peak, indicating that the economy is slowing. A drop of 300,000 would signal a recession.

The unemployment rate, based on the monthly household survey, declined to 4.4% in December, below the typical 5.0% minimum during a recession.

However, employers are cutting back employees’ hours. Average weekly hours worked declined to 34.2 in December, a sign that layoffs are likely to follow.

Employers are also cutting back on temporary help services, another typical sign of a recession.

Average Hourly Earnings and Fed Monetary Policy

Average hourly earnings grew at an annualized rate of 3.9% in December, compared to a 3-month average of 4.0%, a 6-month average of 3.9%, and a 12-month average of 3.8%. Growth rates are nearly double the Federal Reserve’s 2.0% inflation target, reflecting underlying inflationary pressures.

Fed monetary policy is becoming stimulative, with average earnings growth now exceeding the latest Fed funds rate (FFR) target range of 3.5% to 3.75%, suggesting a negative real Fed funds rate. Monetary policy is restrictive (beige below) when FFR is higher than average earnings growth, and stimulative (green) when FFR is lower.

Stimulative monetary policy risks fueling inflation if not offset by deflationary pressures from a contracting economy.

Consumers

Residential housing construction is a major cyclical employer, and declining new housing starts and permits signal an impending economic contraction.

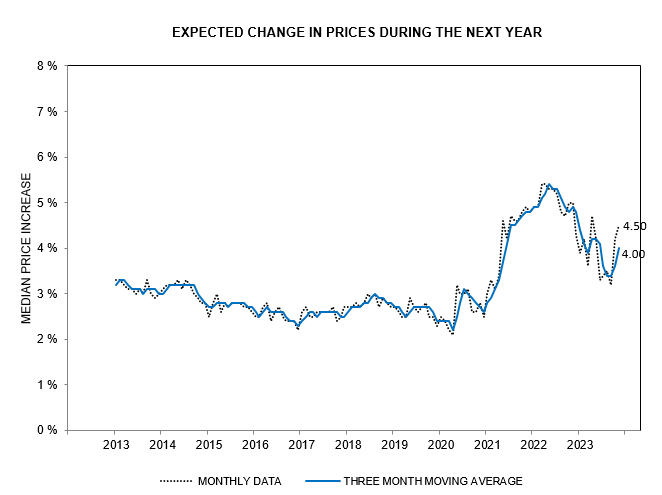

The University of Michigan Index of Consumer Sentiment provides another recession warning, with the 3-month average at a record low since the survey commenced in 1960.

The Index of Current Economic Conditions is similarly at its lowest level in the past 65 years.

Inflation expectations remain elevated, averaging 4.3%, more than double the Federal Reserve’s target rate.

Economy

Aggregate weekly hours worked grew by 0.6% in 2025, suggesting that real GDP growth will likely decline from the 2.3% year-on-year growth in Q3 of last year.

The Philadelphia Fed Index of Coincident Economic Activity grew by 2.15% over the 12 twelve months to November 2025. Values below 2.5% warn of a recession.

Heavy truck sales are also declining, with the 12-month moving average falling to 34.0 thousand units. The decline of more than 10% from the October 2023 high of 43.0 thousand indicates a recession.

ISM Manufacturing

The ISM Manufacturing PMI declined to 47.9% in December, the tenth consecutive month of contraction in the sector.

New orders declined to 47.7% for the sector, indicating a deteriorating outlook.

The Prices Index declined to 58.5%, indicating continued growth in producer prices, although the rate has slowed from the first half of 2025.

ISM Services

The large services sector continues to expand, with the ISM Services PMI rising to 54.4% in December.

However, the Prices Index, at a strong 64.3% in December, indicates that inflationary pressures remain a problem.

Financial Markets

Commercial bank reserves recovered to $3.0 trillion, reflecting improved liquidity in financial markets.

Increased Federal Reserve purchases of Treasury bills under the new Reserve Management Purchases (RMPs) program helped bolster bank reserves.

When the Fed made that announcement in December, it said that RMPs for the month from December 12 to January 12 would amount to $40 billion.

The Fed will announce in a few days the amount of the RMPs to be purchased during the next 30-day period. The amounts will vary by season. The Fed is currently frontloading for April 15 Tax Day, when big liquidity strains are expected. (Wolf Richter)

The Fed’s balance sheet expanded for the first time since 2023, driven by RMPs and a $75 billion increase in the standing repo facility (SRF) on December 31 to support repo market liquidity.

Most of the SRF was repaid the following week, but the secured overnight funding rate (SOFR) still warns of liquidity shortages. An SOFR above the interest rate paid by the Fed on reserve balances (IORB) indicates that the Repo market is prepared to pay a premium to attract funding from commercial banks.

A decline of more than $150 billion in the Treasury General Account at the Fed also helped boost liquidity over the year-end period.

The National Financial Conditions Index from the Chicago Fed continues to indicate loose monetary conditions, declining to -0.5536 on January 2.

A Bitcoin (BTC) recovery above 90,000 also indicates improving liquidity in financial markets. The volatile cryptocurrency is retracing to test the new support level, and respect of 90,000 would confirm improving monetary conditions.

Stocks

The S&P 500 reached a new high, testing resistance at 7000, but declining Trend Index peaks continue to warn of secondary selling pressure.

The Roundhill Magnificent 7 ETF (MAGS) reversed its uptrend relative to the iShares Russell 2000 ETF (IWM), indicating that small-cap stocks are now outperforming mega-cap technology stocks. Market leaders falling behind and no longer leading advances is a typical sign of the final stage of a bull market.

Conclusion

The labor market reports dismal job growth in December, but cyclical sectors of the US economy are shedding jobs, warning of an economic contraction ahead. A decline in average weekly hours worked and in temporary help services indicates that employers are tightening their belts, and layoffs will likely follow.

Average hourly earnings are growing at an annual rate of nearly 4.0% while the federal funds target range is 3.5% to 3.75%. Fed monetary policy risks fueling inflation if not offset by deflationary pressures, indicating that the central bank expects an economic contraction.

Declining cyclical sector indicators, including new housing starts, heavy truck sales, and a tenth consecutive month of contraction in the ISM Manufacturing PMI, all warn of a slowing economy. This bearish outlook is also supported by a slowing Coincident Economic Activity Index and weak annual growth in aggregate hours worked.

The Fed and the US Treasury are doing their best to support financial market liquidity, but Bitcoin at 90,000 continues to warn of weak liquidity.

Small-cap stocks are now outperforming mega-cap technology stocks, a pattern typical of the final stage of a bull market, suggesting that the S&P 500 may struggle to break the 7000 resistance level.

Acknowledgments

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He founded PVT Capital (AFSL number 546090), which provides income and growth strategies to wholesale clients.

Colin also co-founded Incredible Charts and writes the popular Patient Investor newsletter.

Using a top-down approach, Colin identifies macro trends in the global economy and then combines fundamental and technical analysis to evaluate opportunities in sectors that stand to benefit.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.