Bearish divergence warns of tech stock retracement

The US recorded more than 75,000 new COVID19 cases on July 16th. The CCP must be smiling behind their masks after successfully containing last month’s outbreak in Beijing.

Source JHU CSSE

Technology stocks have screamed upwards despite the chaos, but bearish divergence on Twiggs Money Flow now warns of selling pressure. Expect retracement to test support at 2650 on the Dow Jones US Technology Index.

Dow Jones Banks Index is a more realistic representation of the broader US economy. The weak rally has fizzled out, with a Money Flow peak at zero now warning of strong selling pressure. Breach of short-term support at 320 would signal another test of primary support at 270/280.

Government support can only cushion the impact of a massive surge in unemployment for a limited time. Then we will witness the full extent of the damage.

Continued unemployment claims jumped to 17.355 million on July 4th, up by 840,000 from a week earlier. Judging by the rising virus count, further increases are likely.

But that is only the tip of the iceberg.

The latest Department of Labor update shows 32 million people claimed unemployment insurance benefits in all programs for the week ending June 27.

…..21% of the 152.4 million non-farm workforce in February 2020.

Pandemic Unemployment Assistance (PUA) under the CARES Act, signed into law on March 27, 2020 provides benefits to those individuals “not eligible for regular unemployment compensation or extended benefits under state or Federal law or pandemic emergency unemployment compensation (PEUC), including those who have exhausted all rights to such benefits.”

The S&P 500 is inching upwards, reflecting the tug-of-war between technology stocks and the broader market. We expect retracement of the Technology Index to cause another test of support at 3000 (on the S&P 500).

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.

Nasdaq: Devil take the hindmost

I am fond off quoting Jesse Livermore’s maxim “You don’t argue with the tape” but Livermore was a keen student of market conditions and based his decisions on far more than just price action in the market.

We are witnessing a spectacular stock market rally, driven by retail investors and hedge funds piling into the market while institutional investors are sitting on the sidelines.

The Nasdaq 100 broke through resistance at 10,000, new highs signaling a fresh primary advance. Bearish divergence on Twiggs Money Flow index may warn of selling pressure but it is hard to argue with the tape. Only a fall below 9500 would signal another decline and that seems unlikely at present.

Even retail sales (ex food) have recovered sharply, from -15.3% in April to -1.4% in May (annual % gain).

Light vehicle sales are more sluggish but June sales of 13.05 million are still a sizable bounce.

So why are many old investment hands acting with such caution?

We know that the efforts to contain the COVID19 outbreak are struggling, with over 60,000 new cases per day, but the economy still seems in good shape.

Source JHU CSSE

Let’s look at where the money is coming from.

Treasury debt has expanded by more than $3 trillion in the last four months (March 9 – July 9) as the government does everything in its power to cushion the economy from an unprecedented shutdown. Rescuing airlines, bailing out Boeing, emergency business loans, job preservation schemes, and supporting Fed purchases of a wide variety of financial assets to keep the plumbing of financial markets open. Every way they can, government has been flooding the market with money and some of that has found its way to the stock market. Whether through boosting stock purchases, enabling companies to raise debt or boosting consumer spending to buoy up sales, the market is flying on borrowed money.

Steep up-trends like this typically end in a blow-off. A trend is self-reinforcing if rising prices attract more investors who in turn bid up prices even further. A steady influx of new investors is required to sustain the trend, else it dies.

Similar self-reinforcing cycles are evident in nature, where they expand violently outward at an exponential rate until they run out of fuel. The fuel driving the event may differ, from dry tinder in a forest fire, warm ocean temperatures in a hurricane, consumable vegetation in a locust plague, …..or exposed population in a virus outbreak. The cycle expands, feeding on itself, until the fuel is exhausted.

A stock market blow-off is no different. The up-trend will continue for as long as rising prices are able to attract new investors. It will stop when the source of new money dries up. In this case, when Treasury tries to slow the unsustainable growth in federal debt. Then it becomes a case of devil-take-the-hindmost as a preponderance of sellers attempt to offload their stocks on a rapidly shrinking pool of buyers.

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.

COVID19: The new normal

COVID19 looks like it will be with us for some time. The US has to guard against a second wave, destroying any hard-won gains.

Especially with the upsurge in daily cases in Mexico.

Australia has been fortunate to catch the outbreak early.

But international travel is likely to remain restricted for a long time. When you have new outbreak hotspots like Brazil….

and Pakistan appearing on the radar.

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.

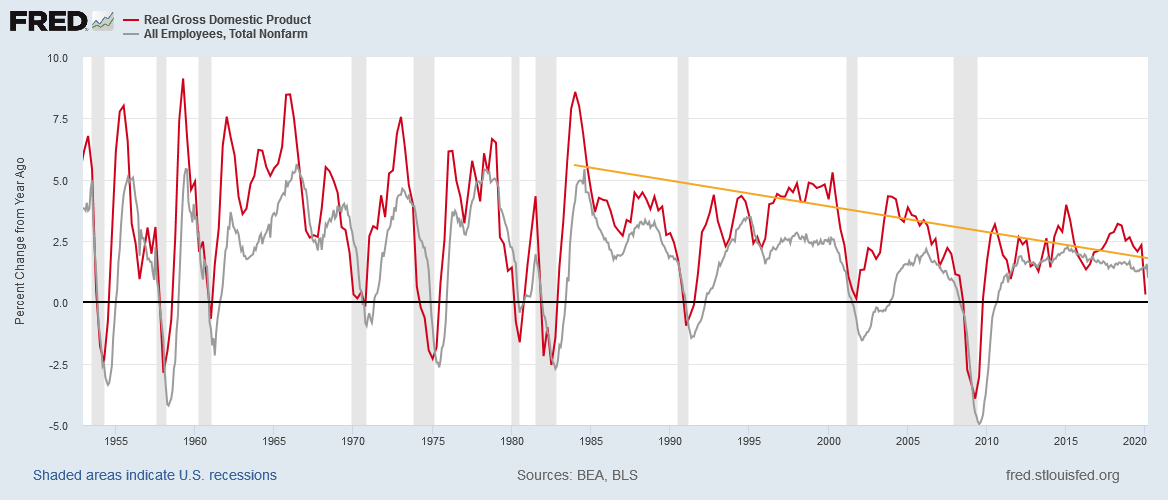

Jobs and GDP growth

The view is often promoted that low GDP growth over the past decade is caused by low interest rates and balance sheet expansion (QE) by central banks. That is putting the cart before the horse. Central banks have tried to stimulate their economies, with massive QE and low interest rates, because of low GDP growth. Not the other way around.

The real cause of low GDP growth is low job growth, as the chart below illustrates.

[click here for full screen image]

{kind=link}

Offshoring jobs means offshoring growth.

The last time that the US had employment growth above 5.0% is 1984 which also the last time that we saw real GDP growth at 7.5%. Since then, job growth has progressively weakened — and GDP with it.

In the last decade, employment growth peaked at 2.27% and GDP at 3.98% in Q1 of 2015.

We now expect job growth to fall to -20% in April, four times the -5% trough in 2009, and a sharp GDP contraction.

How long the recession/depression will continue is uncertain. But, in the long-term, it is unlikely that the US can achieve +5% real GDP growth unless employment growth recovers close to +3.0%.

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.

No V-shaped Recovery

Initial jobless claims in the US for the 6 weeks to April 25th exceed 30 million.

That will take unemployment above 20%, with total jobs falling to levels last seen in 1997, and more job losses still to come.

Employment is the key to economic recovery. While unemployment is high, consumer spending will stay low and the economy will struggle. Companies may receive bailouts and the Fed will keep financial markets awash with liquidity but that does not help falling sales.

Be prepared. April employment numbers are going to be ugly. Expect some turbulence.

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.

Crude oil: Opportunities and value traps

On the weekend we wrote that the bottom had fallen out of the oil market after Nymex crude broke support at $20 per barrel.

Now, the previously unimaginable has occurred, with Nymex Light Crude falling below zero for the first time in history, closing at -$13.10 per barrel with reports of intra-day lows at -$37.63.

From The Age:

“Traders are still paying $US20.43 for a barrel of US oil to be delivered in June, which analysts consider to be closer to the “true” price of oil. Crude to be delivered next month, meanwhile, is running up against a stark problem: traders are running out of places to keep it, with storage tanks close to full amid a collapse in demand as factories, automobiles and airplanes sit idled around the world.

Tanks at a key energy hub in Oklahoma could hit their limits within three weeks, according to Chris Midgley, head of analytics at S&P Global Platts. Because of that, traders are willing to pay others to take that oil for delivery in May off their hands, so long as they also take the burden of figuring out where to keep it.”

Brent Crude is trading at $25.57 per barrel but a Trend Index peak deep below zero warns of similar strong selling pressure.

Outlook

Crude oil production is still in a long-term up-trend. Low prices may present opportunities to buy cyclical stocks at historically low prices.

The Oil & Gas sector has plunged as expected.

Oil infrastructure is also suffering from low activity levels.

Energy-consuming industries, however, may benefit from lower oil prices.

Transport

Transport is the biggest consumer of crude oil products.

If we break usage down by fuel types, the largest is diesel/gas, followed closely by motor gasoline, with jet kerosene significantly smaller.

Airlines which have suffered from a massive drop in air travel.

While delivery services (formerly air freight) are suffering from the collapse of global trade.

So is marine transport.

But trucking is holding up well.

Construction Materials

Crude oil runs a distant second to coal as the chief energy source for cement production.

But the industry is a heavy transport user and should benefit from lower oil prices.

Mining

Mining is also likely to benefit from lower extraction and transport costs.

Forestry & Paper

Forestry is another heavy fuel user.

Chemicals & Plastics

Basic chemicals (including fertilizers) are the largest industrial consumer of crude oil.

Specialty chemicals are also largely oil-based.

Aerospace & Automobiles

Aerospace, laid low by problems at Boeing (BA), has been floored by a massive downturn in the airline industry and will take a long time to recover.

Automobiles have so far stood up well because of stellar performance from the likes of Tesla (TSLA).

But the sting is in the tail. Light vehicle sales have plummeted.

Low vehicle sales and less travel also means lower tire sales.

Oil Producers in Affected Regions

The IEA graph below shows producing regions that are uneconomic at varying prices/barrel (x-axis). If we take $25/barrel as the average over the next two years, North American producers would suffer the most, followed by Asia-Pacific and Latin America.

Middle-Eastern producers enjoy the lowest extraction costs and are mostly still profitable at lower prices.

Avoiding Value Traps

Value opportunities abound in industries that are badly affected by the economic contraction and falling crude prices — as well as by those industries that stand to benefit from low oil prices. Some affected industries, however, are going to struggle to survive without state assistance.

The problem with value stocks is that, although they may seem cheap, prices can fall a lot further. That is why we use both technical and fundamental analysis to evaluate opportunities.

There are many stocks that are trading well below our assessment of fair value at present but we will not buy until the technical outlook turns bullish. It takes plenty of patience. But helps to avoid value traps.

The stock market remains an exceptionally efficient mechanism

for the transfer of wealth from the impatient to the patient.~ Warren Buffett

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.

Coronavirus: “We are all Keynesians now”

An economic depression requires a 10% (or more) decline in real GDP or a prolonged recession that lasts two or more years.

The current contraction, sparked by the global coronavirus outbreak, is likely to be severe but its magnitude and duration are still uncertain. After an initial spike in cases, with devastating consequences in many countries — both in terms of the number of deaths and the massive economic impact — the rate of contagion is expected to drop significantly. But we could witness further flare-ups, as with SARS.

Development of a vaccine is the only viable long-term defense against the coronavirus but health experts warn that this is at least 12 to 18 months away — still extremely fast when compared to normal vaccine development programs.

The economic impact may soften after the initial shutdown but some industries such as travel, airlines, hotels, cruise lines, shopping malls, and cinemas are likely to experience lasting changes in consumer behavior. The direct consequences will be with us for some time. So will the indirect consequences: small business and corporate failures, widespread unemployment, collapsing real estate prices, and solvency issues within the financial system. The Fed is going to be busy putting out fires. While it can fix liquidity issues with its printing press, it can’t fix solvency issues.

There are three key factors that are likely to determine whether countries end up with a depression or a recession:

1. Leadership during the crisis

Many countries were caught by surprise and the rapid spread of the virus from its source in Wuhan, China. South Korea, Singapore and Taiwan were best prepared, after dealing with the SARS outbreak in the early 2000s. Extensive testing, tracing and an effective quarantine program helped South Korea to bring the spread under control, after initially being one of the worst-hit.

South Korea: Initial Cases of Coronavirus COVID-19 (JHU)

The World Health Organization (WHO) did little to help, delaying declaration of a pandemic to appease the CCP. Economic and political self-interest has been the root cause of many failures along the way, including China’s failure to alert global authorities of the outbreak (they had already shut down Wuhan Naval College on January 1st). But this was aided by failure of many leaders to heed warnings from infectious disease experts in late January/early February. When they finally did wake up to the threat, many were totally unprepared, resulting in a massive spike in cases across Europe and North America.

Testing is a major bottleneck, with the FDA fast-tracking approval of new tests, but production volumes are still limited. Abbott recently obtained FDA approval for a new 5-minute test kit that can be used in temporary screening locations, outside of a hospital, but production is currently limited to 50,000 per day. A drop in the ocean. It would take 6 months to produce 9 million kits for New York alone.

USA: Initial Cases of Coronavirus COVID-19 (JHU)

UK: Initial Cases of Coronavirus COVID-19 (JHU)

Germany: Initial Cases of Coronavirus COVID-19 (JHU)

Italy: Initial Cases of Coronavirus COVID-19 (JHU)

Widespread testing and tracing, social-distancing, and effective quarantine methods have enabled some countries to flatten the curve. Australia may be succeeding in reducing the number of new cases but inadequate testing and tracing could lead to further flare-ups. One of the biggest dangers is asymptomatic carriers who can infect others. Flattening the curve is the first step, but keeping it flat is essential, and requires widespread testing and tracing.

Australia: Initial Cases of Coronavirus COVID-19 (JHU)

The curves for North America and Europe remain exponential. They may even spike a lot higher if hospital facilities are overrun. Success in flattening the curve is critical, not just in minimizing the number of deaths but in containing the economic impact.

2. Economic rescue measures during the crisis

Rescue measures amounting to roughly 10% of annual GDP have been introduced in several countries, including the US and Australia, to soften the economic impact of the shutdown. More Keynesian stimulus may be needed if the coronavirus curve is not flattened. Layoffs have spiked and many small businesses will be unable to recover without substantial support.

3. Economic stimulus after the crisis

This is not a time for half-measures and the $2 trillion infrastructure program proposed in the US is also appropriate in the circumstances. Australia is likely to need a similar program (10% of GDP) but it is essential that the money be spent on productive infrastructure assets. Productive assets must generate a market-related return on investment ….or generate an equivalent increase in government tax revenue but this is much more difficult to measure. Investment in unproductive assets would leave the country with a sizable debt and no ready means of repaying it (much like Donald Trump’s 2017 tax cuts).

Conclusion

Social-distancing and effective quarantine measures are necessary to flatten the curve but widespread testing and tracing is essential to prevent further flare-ups. Development of a vaccine could take two years or more. Until then there is likely to be an on-going economic impact, long after the initial shock. This is likely to be compounded by a solvency crisis in small and large businesses, threatening the stability of the financial system. The best we can hope for, in the circumstances, is to escape with a recession — less than 10% contraction in GDP and less than two year duration — but this will require strong leadership, public cooperation and skillful prioritization of resources.

—–

“We are all Keynesians now.” ~ Richard Nixon (after 1971 collapse of the gold standard)

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.

Lessons from the Panic of 1907

I have read The Panic of 1907 (by Robert Bruner & Sean Carr) four or five times — I read it at every market crash.

The crash occurred more than 100 years ago and is one of many banking crises that beset the United States in the 19th and early 20th century. What made 1907 stand out is that the financial system was saved by the leadership of a private individual, John Pierpont Morgan, head of the banking firm that later became known as J.P. Morgan & Co. Without the 70-year old Morgan’s force of will, the entire financial system would have imploded.

John Pierpont Morgan – source: Wikipedia

The crisis led to formation of the Federal Reserve Bank in 1913. The US had not had a central bank since President Andrew Jackson withdrew the charter for the second Bank of the United States in 1837. Bank clearing houses prior to 1913 were private arrangements created by syndicates of banks and were poorly-equipped to deal with the challenges of a banking crisis.

The lessons of 1907 are still relevant today. The authors of the book suggest that “financial crises result from a convergence of forces, a ‘perfect storm’ at work in financial markets.”

They identify seven elements that converged to create a perfect storm in 1907:

- Complex Financial Architecture makes it “difficult to know what is going on and establishes linkages that enable contagion of the crisis to spread.”

- Buoyant Growth. “Economic expansion creates rising demands for capital and liquidity and ….excessive mistakes that eventually must be corrected.”

- Inadequate Safety Buffers. “In the late stages of an economic expansion, borrowers and creditors overreach in their use of debt, lowering the margin of safety in the financial system.”

- Adverse Leadership. “Prominent people in the public and private spheres implement policies that raise uncertainty, which impairs confidence and elevates risk.”

- Real Economic Shock. “Unexpected events hit the economy and financial system, causing a sudden reversal in the outlook of investors and depositors.”

- Undue Fear, Greed and other Behavioral Aberrations. “….a shift from optimism to pessimism that creates a self-reinforcing downward spiral. The more bad news, the more behavior (erupts) that generates bad news.”

- Failure of Collective Action. “The best-intended responses by people on the scene prove inadequate to the challenge of the crisis.”

Compare these seven elements to the current crisis in March 2020:

Complex Financial Systems

The global financial system is far more complex than the gold-based financial system of 1907. Regulation has not kept pace with the growth in complexity, with many products designed to avoid regulation and lower costs. The ability to build firebreaks to stop the spread of contagion in unregulated or lightly regulated areas of the financial system is severely limited. And that is where the fires tend to start.

In 1907 the fire started with poorly regulated trust companies that dominated the financial landscape: making loans, receiving deposits, and operating as an effective shadow-banking system. A run on trust companies threatened to engulf the entire financial system.

In 2020 it started with hedge funds leveraged to the hilt through repo markets but soon threatened to spread to other unregulated (or lightly regulated) areas of our shadow banking system:

- Leveraged hedge funds

- Risk parity funds

- International banks lending and taking deposits in the unregulated $6.5 trillion Eurodollar market (these banks are offshore and outside the Fed’s jurisdiction).

- Money market funds

- Muni funds

- Commercial paper markets

- Leveraged credit

- Bond ETFs

Many of these offer the attraction of low costs and higher returns, often enhanced through leverage, but what investors are blind to (or choose to ignore) are the risks from lack of proper supervision and the lack of liquidity when money is tight.

Maturity mis-match is often used to boost returns. Short-term investors are channeled into long-term securities such as Treasuries, corporate bonds, munis or credit instruments, with the promise of easy sale or redemption when they require their funds. But this tends to fail when there is a liquidity squeeze, forcing a sell-off in the underlying securities and steeply falling prices.

Rapid Growth

We all welcome strong economic growth but should beware of the attendant risks, especially when financial markets are administered more stimulants than a Russian weightlifter for purely political ends.

Excessive use of Debt

Corporate borrowings are far higher today and rising debt has warned of a coming recession for some time.

Public debt is growing even faster, with US federal debt at 98.6% of GDP.

Adverse Leadership

In the early 1900s, President Teddy Roosevelt led a populist drive to break the big money corporations through Anti-Trust prosecutions. This cast a shadow of uncertainty that fueled the sudden reversal in investor sentiment.

In 2020, we have another populist in the White House. Frequent changes in direction, spats with allies, imposition of trade tariffs, impeachment efforts by Congress, and a heavy-handed approach to trade negotiations have all elevated the level of uncertainty.

Economic Shock

The great San Francisco earthquake and fire of 1906 created an economic shock that was felt across the Atlantic. The earthquake ruptured gas mains, setting off fires, while fractured water mains hampered firefighting. Over 80% of the city was destroyed. Much of the insurance was carried in London and Europe and led to a sell-off of securities in order to meet claims. The Bank of England became increasingly concerned about the outflow of gold from the UK and hiked its benchmark interest rate from 3.5% to 6.0%. London was then the hub of global financial markets and money became tight.

In 2020 we have the coronavirus impact on global manufacturing, services and financial systems: the mother of all demand and supply shocks.

Undue Fear and Greed

Collapse of highly leveraged ventures in 1907 — with an attempted short squeeze on United Copper shares by connected corporations, banks and broking houses — stirred fears that a leading Trust company was going to fail. The panic soon spread and started a run on a number of trust companies.

A spike in the repo rate in September last year revealed that hedge funds had used repo to leverage their relatively meager capital into a rumored $650 billion exposure to US Treasuries. The Fed had to dive in with liquidity to settle the repo markets, lifeblood of short-term funding by primary dealers. But financial markets were on edge and concerns about funding difficulties in the unregulated $6.5 trillion offshore Eurodollar market and leveraged credit in the US started to grow. But the coronavirus outbreak in Europe and North America was the eventual spark that set off the conflagration.

Failure of Collective Action

Tust companies failed to organize an effective defense in 1907 against a run on their largest member, The Knickerbocker Trust Company, fueling a panic that threatened to engulf other trusts. Responding to appeals for help, J.P. Morgan intervened and marshaled the banking industry and surviving trusts to mount an effective defense.

Today that role falls to the Federal Reserve. Chairman Jay Powell moved quickly and purposefully to flood financial markets with liquidity, but the Fed was forced to reach far outside their normal ambit — increasing dollar swap lines with foreign central banks (to supply liquidity to international banks operating in the Eurodollar market) and providing liquidity to money market funds, muni funds, commercial paper markets, bond funds, hedge funds (through repo markets) and more. In effect, the Fed had to bail out the shadow banking system.

One thing that strikes me about financial crises is that each one is different, but some things never change:

- artificially low interest rates;

- rampant speculation;

- excessive use of debt;

- unregulated and highly leveraged shadow-banking with hidden linkages through the financial system;

- financial engineering (the latest examples are leveraged credit and covenant-lite loans, hedge funds running leveraged arbitrage, risk parity funds with targeted volatility, and management using stock buybacks to enhance earnings per share, support prices and boost their stock-based compensation);

- misuse of fiscal stimulus (to fund corporate tax cuts while running a $1.4 trillion fiscal deficit);

- misuse of monetary policy (cutting interest rates when unemployment was at record lows);

- yield curve inversion; and

- misallocation of investment (to fund unproductive assets)

Jim Grant (Grant’s Interest Rate Observer) sums up the problem:

“The Fed has intervened at ever-closer intervals to suppress the symptoms of misallocation of resources and the mis-pricing of credit. These radical interventions have become ever-more drastic and the ‘doctor-feel-goods’ of our central banks have worked to destroy the pricing mechanism in credit.

….[credit and equity markets] have become administered government-set indicators, rather than sensitive- and information-rich prices… and we are paying the price for that through the misallocation of resources…..

Is there no salutary role for recessions and bear markets? …..they separate the sound from the unsound, they separate the well-financed from the over-leveraged and if we never have these episodes of economic pain, we will be much the worse for it.”

We haven’t learned much at all in the last 100 years.

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.

Dow: Not so fast WSJ

We were surprised to receive this from The Wall Street Journal this morning:

Markets Alert

Dow Industrials Rally, Ending Bear Market

A new bull market has begun. The Dow Jones Industrial Average has rallied more than 20% since hitting a low three days ago, ending the shortest bear market ever.

That is news to us. A 20% reversal is a quick rule of thumb used by brokers. It is not part of Dow Theory. To suggest that we are now in a bull market is ludicrous.

Dow Theory tracks secondary movements in the index which last from ten to sixty days (Nelson, 1903). Only if the secondary movement forms a higher trough followed by a higher peak does that signal reversal to an up-trend. And the same pattern has to occur on the Transport Average to confirm the change.

A three-day rally is a normal part of a bear market and, with volatility near record highs, it is likely that some rallies are going to reach 20 per cent.

Bear markets are more volatile than bull markets. You can see this from the volatility spikes above in 1991, 2000-2003, 2008, and 2020. Stocks go up on the escalator and down in the elevator.

According to data from S&P Dow Jones Indices, most days with the biggest gains occur in a bear market. Eighteen of the top twenty biggest daily % gains on the Dow occurred in a bear market. Only two (marked in blue) were in a bull market.

The largest gains in the 1930s bear market were as high as 15% in a single day!

Interesting that eighteen of the top twenty biggest daily % losses on the Dow also occurred in a bear market (red).

That is because volatility is a lot higher in bear markets than in bull markets.

So expect big moves in both directions.

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.

You must be logged in to post a comment.