Ernest Hemingway’s 1926 novel The Sun Also Rises contains this snippet, fondly referred to as the Hemingway Law of Motion:

“How did you go bankrupt?” Bill asked.

“Two ways,” Mike said. “Gradually and then suddenly.”

Niels Clemens Jensen at Absolute Return Partners has published an interesting piece on de-dollarisation. He believes that the US can get away with a lot more bad policy choices than the UK because the Dollar is the global reserve currency:

British investors learned (the hard way) what the consequences are when your Prime Minister mistakenly believes that large-scale tax cuts can be financed with borrowings. Liz Truss tried to do that in October 2022 and, within days, she was history.

You may wonder why the Americans can get away with such things when the British cannot, and the answer is simple. The Americans benefit from the US dollar’s reserve currency status, which means that foreign investors hold massive amounts of US debt but little UK debt.

However, poor policy choices have reduced the Dollar’s role as the global reserve currency. We are past the tipping point, and the shrinkage rate is accelerating.

I am not at all suggesting that the US is about to turn into the next Argentina. Nor am I saying that we are about to witness a repeat of the Liz Truss narrative. The US economy possesses so much talent and so many resources that an awful lot of bad decisions have to be made, before we are even close to an Argentina-like situation.

However, what I want to say with this is that the ongoing de-dollarisation will change the name of the game, and Americans had better realise that the rules are different, if you are no longer the hyperpower of the world.

Despite all Trump’s warnings, a change is underway…..

De-Dollarization

The watershed in de-dollarization may have been in 1971 when Richard Nixon removed the Dollar from the gold standard. However, the rot started earlier, with Lyndon Johnson’s guns-and-butter policies of the 1960s. Johnson prioritized expanding welfare with his Great Society programs but was caught up in the Cold War arms race and the Vietnam War. The conflicting demands strained the US budget, with rising deficits eroding confidence in the Dollar.

President Charles de Gaulle started a run on the Dollar in 1965 when he announced France’s intention to exchange US dollar reserves for gold at the official exchange rate. The French Navy sailed across the Atlantic to collect French gold, setting off demands by other states. This forced US President Nixon to end the convertibility of the Dollar to gold in August 1971 to prevent erosion of US gold reserves.

Removing the gold standard opened the Dollar to currency manipulation. Japan led the way, accumulating large reserves in US Dollars. The weak Yen gave Japanese manufacturers an enormous advantage over their US counterparts in export markets and the US domestic market.

Japan’s example was followed by South Korea, Germany, and China, forcing the US to run large fiscal and current account deficits to accommodate the excess savings of trading partners.

The supposed benefit of the strong Dollar—low interest rates—fed ballooning debt and rising instability as strains on the US economy increased.

The US net international investment position deteriorated from the world’s largest creditor to the world’s largest debtor.

The manufacturing sector was dealt a devastating blow, with industrial output plummeting as industry shed millions of jobs. The chart below reflects US manufacturing output relative to real GDP since the early 1970s.

The Tipping Point

Historian Niall Ferguson argues that a tipping point is reached when the cost of servicing government debt exceeds the defense budget. According to Ferguson, no hegemon in history has ever restored its previous supremacy after reaching that tipping point. When your economy can no longer support your military, however dominant it is, it becomes only a matter of time.

Conclusion

The typical complacent response is that the United States is far too powerful to be challenged, and there is no real substitute for the Dollar as global reserve currency or US Treasuries as global reserve asset. However, decades of economic mismanagement have eroded confidence in the Dollar as a store of value. Geopolitical blunders also squandered much of the advantage accumulated from the post-WWII Pax Americana.

The decline in American power over the past two decades is likely to seem gradual compared to its eventual collapse. Applying Hemingway’s Law of Motion, the change should come quickly once the tipping point is reached.

The Pax Romana lasted several centuries, but its decline was swift after Rome’s economic dominance crumbled. British dominance lasted from the end of the Napoleonic Wars in 1815 to the outbreak of the First World War in 1914. Britain’s navy still ruled the waves for another three decades, but its economic decline had already begun.

President-elect Trump has promised to reverse the US economic slide. Unfortunately, his chance of getting that right is closer to William Buckley1 than Lyndon Johnson or Richard Nixon.

Please note that this does not necessarily mean that the US central role in the global economy will be replaced by China, which faces its own set of challenges. What is more likely is a destabilizing vacuum, with rival states jostling for power and riding roughshod over their weaker neighbors. Ancient Greek historian Thucydides observed, in his History of the Peloponnesian War (c. 400 BC), on the conflict between Athens and Sparta:

The strong do what they will and the weak suffer what they must.

In times of uncertainty, demand for gold rises.

Acknowledgments

- Niels Clemens Jensen, Absolute Return Partners: The Finite Life of Hyperpowers

- Ben Steil & Elisabeth Harding, Council on Foreign Relations: For the First Time, the US. Is Spending More on Debt Interest than Defense

- Reason: The National Debt Is Crossing an Ominous Line

Notes

- In Australian vernacular, “Buckley’s chance” refers to William Buckley, who escaped from a convict ship in 1803 and was left presumed dead when the ship drew anchor and sailed onwards to Sydney. Thirty years later, Buckley turned up to greet the first ships arriving to settle the Port of Melbourne, having survived in the bush against improbable odds, supported by indigenous tribes.

Colin Twiggs is a former investment banker with almost 40 years of experience in financial markets. He co-founded Incredible Charts and writes the popular Trading Diary and Patient Investor newsletters.

Using a top-down approach, Colin identifies key macro trends in the global economy before evaluating selected opportunities using a combination of fundamental and technical analysis.

Focusing on interest rates and financial market liquidity as primary drivers of the economic cycle, he warned of the 2008/2009 and 2020 bear markets well ahead of actual events.

He founded PVT Capital (AFSL No. 546090) in May 2023, which offers investment strategy and advice to wholesale clients.

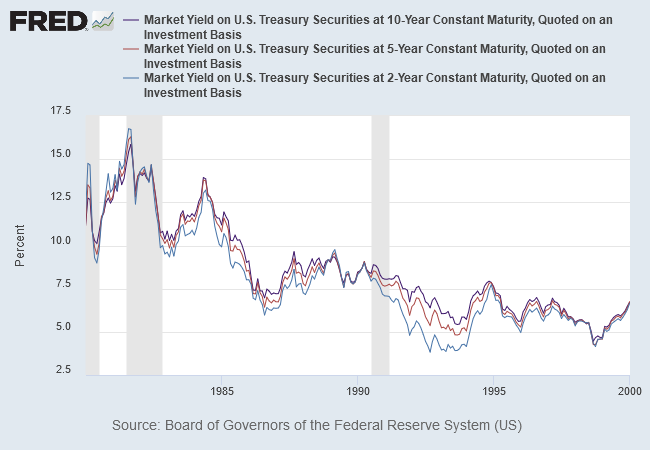

By the graph, defense & interest expenditures almost crossed in 1997 before interest expenditure fell. Why?

UST yields were declining

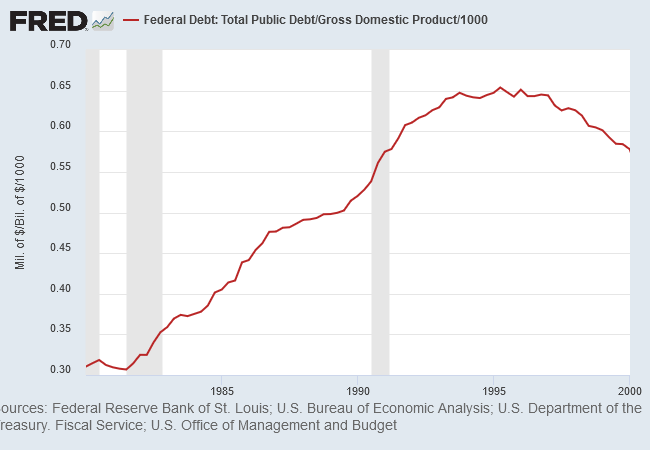

However, federal debt more than doubled due to Reagan’s trickle-down economics in the 1980s.

Defense spending also dipped as a percentage of total gov. spending in the 1990s.