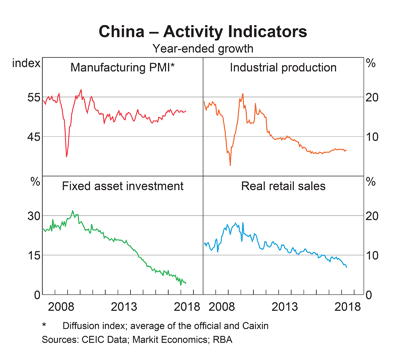

Reuters says that export orders are falling and the contraction is expected to worsen in coming months:

Beijing is widely expected to announce more support measures in coming weeks to avert the risk of a sharper economic slowdown as the United States ratchets up trade pressure……

On Friday, the central bank cut banks’ reserve requirements (RRR) for a seventh time since early 2018 to free up more funds for lending, days after a cabinet meeting signaled that more policy loosening may be imminent.

August exports fell 1% from a year earlier, the biggest fall since June, when it fell 1.3%, customs data showed on Sunday. Analysts had expected a 2.0% rise in a Reuters poll after July’s 3.3% gain.

That’s despite analyst expectations that a falling yuan would offset some cost pressure and looming tariffs may have prompted some Chinese exporters to bring forward or “front-load” U.S.-bound shipments into August, a trend seen earlier in the trade dispute…..

Among its major trade partners, China’s August exports to the United States fell 16% year-on-year, slowing sharply from a decline of 6.5% in July. Imports from America slumped 22.4%.

Many analysts expect export growth to slow further in coming months, as evidenced by worsening export orders in both official and private factory surveys. More U.S. tariff measures will take effect on Oct. 1 and Dec. 15.

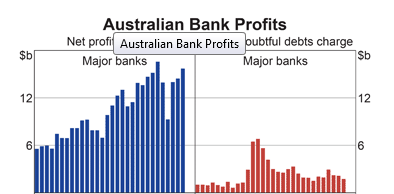

Banks are suffering a liquidity squeeze:

The PBoC says the new cuts will release RMB 900 billion of liquidity. That’s more than the RMB 800 billion and RMB 280 billion released by the January and May cuts, respectively. (Trivium China)

Consumer confidence is ebbing.

China’s response to tariffs has annoyed the Trump administration, making prospects of a trade deal even more remote.

China’s response to U.S. trade actions appears to reflect a cynicism about the efficacy of democracy. Beijing’s strategy appears calibrated to exploit the fact that the American people elect the head of their government, by attempting to influence how the American people will vote. In effect, it seems to be gambling on its ability to turn American democracy against itself.

At the center of China’s responses are the tit-for-tat tariffs intended to hurt American farmers, a constituency that tends to support President Donald Trump and to live in crucial swing states. These tariffs appear designed to deliver political pain in the U.S., not to produce any economic benefit for China. China’s other political meddling, as Vice President Mike Pence recently laid out, includes attempts at interference in the 2018 U.S. midterm elections. Recent targets of Chinese Communist Party influence campaigns also include state and local governments, Congress, academia, think tanks, and the business community. (The Atlantic)

A massive increase in stimulus is the likely eventual outcome, focused on housing and infrastructure. That would fuel demand for raw materials such as iron and steel.

If not, expect a sharp drop in imports to impact on China’s major trading partners.

You must be logged in to post a comment.