August labor stats, released today, point to low real GDP growth for Q3. Growth in weekly hours worked came in at a low 1.09% and GDP is likely to follow.

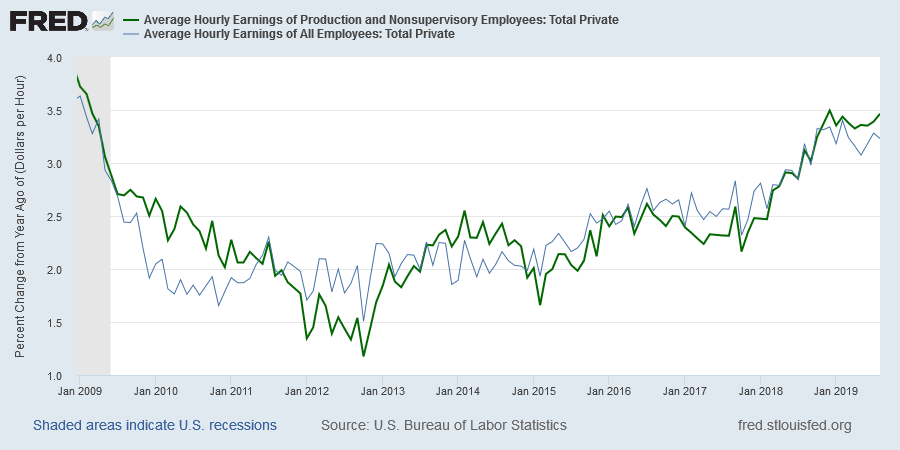

While inflation is not the primary concern at the Fed right now, rising annual hourly wage rate growth (3.46% for total private) flags an increase in underlying inflationary pressure. This may make the Fed more hesitant about cutting rates despite Donald Trump’s tweet storm.

Most important is the continued decline in annual payroll growth. At 1.38% for August, further weakness is likely and a fall below 1.0% would warn of an economic slow-down.

The S&P 500 is headed for another test of resistance at 3000. The Trend Index oscillating above zero for the last 9 months indicates buying pressure but I expect strong resistance at 3000. Upside is limited while downside risks are expanding.

Semiconductors are doing better than expected, despite the trade war, but I suspect will weaken when the surge in orders ahead of tariffs tails off.

Retail has stalled since late 2018 and bearish divergence on the Trend Index suggests selling pressure.

Automobiles, in a decline since 2017, have rallied over the last 6 months. But, again, further weakness is expected.

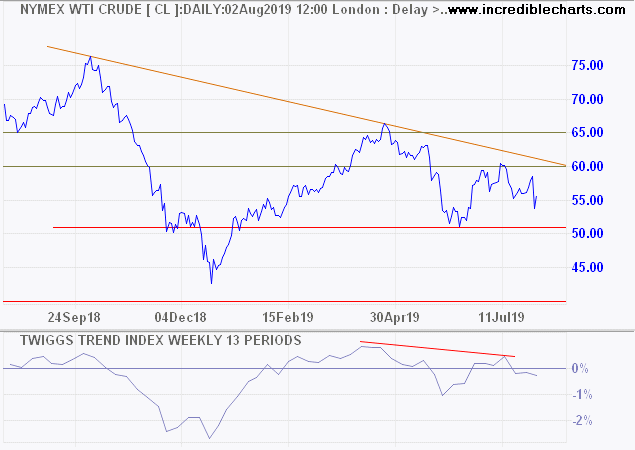

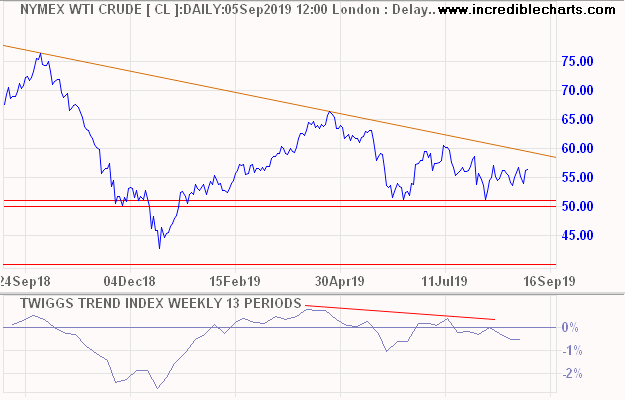

On the global front, weak crude oil prices flag an anticipated slow-down in the global economy. Breach of support at $50/$51 per barrel would be a strong bear signal, warning of a decline to $40 per barrel.

We maintain our bearish outlook and have reduced equity exposure for international stocks to 40% of portfolio value.