There is much talk in the media of a multipolar world, with the split between the West and the BRICS, led by China & Russia. That may be relevant in the long-term but the immediate challenge for investors is a bi-polar world, where some markets are rallying strongly while others are collapsing. Even within the US market, we have some sectors rallying while others are collapsing.

The S&P 500 is still in a bear market but the index has rallied to test resistance between 4200 and 4300. Breakout would confirm the bull signal from 250-day Rate of Change crossing to above zero.

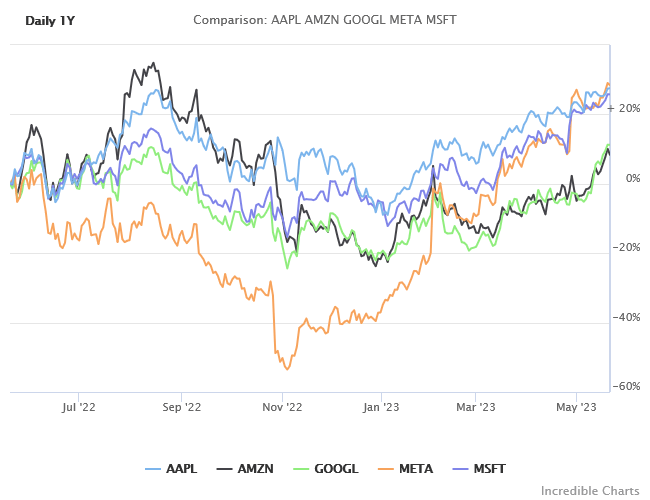

The big 5 technology stocks — Apple, Amazon, Alphabet (GOOGL), Meta Platforms, and Microsoft — have all rallied strongly since the start of 2023.

Volatility is elevated but declining peaks on Twiggs Volatility (21-day) suggest that this is easing.

However, the rally is concentrated in big tech stocks, with small caps struggling to hold above support. The Russell 2000 iShares ETF (IWM) is testing the band of support between 164 and 170. Breach of support would signal a second downward leg in the bear market.

The Treasury yield curve is also inverted, with the ever-reliable 10-Year minus 3-Month spread at its lowest level (-1.49%) since 1981. Recessions tend to only occur after the spread recovers above zero — when the Fed starts cutting short term rates — which tells us that the recession is only likely to arrive in 2024.

The longer than usual lag may be the result of the “pig in the python” — a massive surge in liquidity injected into financial markets during the pandemic.

We are already seeing cracks in the dyke as liquidity starts to recede. Regional banks are in crisis, caused by the sharp hike in interest rates and the collapse in value of their “most secure” assets. Risk-weighted capital ratios are meaningless when bank investments in Treasury and Agency securities — which enjoy the lowest risk weighting — fall sharply in value. True levels of leverage are exposed and threaten bank solvency.

The S&P Composite 1500 Regional Banks Index ($XPBC) is testing support at 75 after a sharp decline. Not only do regional banks have solvency problems, caused by losses on Treasury and Agency investments, many are also over-exposed to commercial real estate (CRE) which faces a major fall in value, primarily in the office sector as demand for office space shrinks due to the shift to work-from-home after the pandemic.

There is always more than one cockroach — as Doug Kass would say — and regional banks are also threatened by a margin squeeze. Short-term rates have surged to higher than long-term rates, pressuring net interest margins. Banks are funded at the short-end and invest (and lend) at the long-end of the yield curve.

The Fed is unlikely to solve the regional bank problem easily, especially with the political impasse in Congress — needed to support any increase in deposit guarantees.

Commodities

Falling commodity prices warn that the global economy is contracting.

Brent crude is in a bear market, testing support at $70 per barrel. But US cude purchases — to re-stock their strategic petroleum reserve (SPR) — may strengthen support at this level.

Copper broke support at $8500/tonne, signaling another test of $7000. Sometimes referred to as “Dr Copper” because of its “PhD in economics”, the metal has an uncanny ability to predict the direction of the global economy.

We use the broader Dow Jones Industrial Metals Index ($BIM) to confirm signals from Copper. The base metals index breached secondary support, at 167, warning of a test of primary support at 150.

Iron ore has also retraced, testing support at $100/tonne. Breach would warn of another test of $80.

Dollar & Gold

The Dollar is also in a bear trend, testing support at 101. The recent rally in our view is simply a “dead cat bounce”, with another test of support likely. Breach would warn of another primary decline in the Dollar.

Gold is in a bull market as the Dollar weakens. Dollar Index breach of 101 would likely cause a surge in demand for Gold, with breakout above $2050 signaling another primary advance — with a medium-term target of $2400 per ounce.

Australia

The ASX 200 recent (medium-term) bull trend is losing steam, with the index ranging in a narrow band between 7200 and 7400 since April.

Breakout from that narrow band will provide a strong indication of future direction. Breach of 7200 is, in our view, far more likely — because of weakness in global commodity prices — and would warn of another test of primary support between 6900 and 7000.

The All Ordinaries Gold Index (XGD), however, is in a strong bull trend. Respect of support between 6900 and 7000 would strengthen the signal, while breakout above the band of resistance (7500 – 7700) would signal another primary advance, with a medium-term target of 8200.

Conclusion

The US market is bi-polar, with large technology stocks leading a rally, while small caps and regional banks are struggling. The lag between an inverted yield curve and subsequent recession may be longer than usual because of the “pig in the python” — large injections of liquidity into financial markets during the pandemic.

Commodities are in a bear market, with falling crude and base metals warning of a global recession.

The Dollar is weakening and we expect a primary advance in Gold — with a medium-term target of $2400 per ounce — if the Dollar Index breaks support at 101.

The ASX medium-term rally is weakening and breach of 7200 would warn of another test of primary support. Two major influences are global commodity prices and major Wall Street indices.

Our outlook remains bearish despite the rally in the US technology sector. We are underweight in growth, cyclical and real estate sectors and overweight in gold, silver, defensive stocks, critical materials, cash, money market funds and short-term interest-bearing securities.