We are witnessing the transition from a bull to a bear market.

I subscribe to Jesse Livermore’s maxim (emphasis added):

“I began to see more clearly—perhaps I should say more maturely—that since the entire list moves in accordance with the main current…. Obviously the thing to do was to be bullish in a bull market and bearish in a bear market. Sounds silly, doesn’t it? But I had to grasp that general principle firmly before I saw that to put it into practice really meant to anticipate probabilities. It took me a long time to learn to trade on those lines.”

The second part of that quote is equally important. You determine whether a market is bullish or bearish by “anticipating probabilities”. Don’t take signals from the charts in isolation. You have to study general conditions.

Livermore gives a classic example in Reminiscences of a Stock Operator of how he anticipated a bear market in 1906 after the Boer War in South Africa had drained Britain’s coffers and the San Francisco earthquake led to massive insurance payouts, forcing insurers to liquidate large swathes of their investment portfolios. But he was wiped out as the market repeatedly rallied. He persisted and eventually was proved right when large rail stocks announced new stock issues. The fact that the issues were structured as instalment issues, with only a down-payment needed to acquire the stock, alerted Livermore that there was not enough liquidity in the market to absorb the stock issues. His broker extended him a line of credit and…

“I profited by my earlier and costly mistakes and sold more intelligently. My reputation and my credit were reestablished in a jiffy. That is the beauty of being right in a broker’s office, whether by accident or not. But this time I was cold-bloodedly right, not because of a hunch or from skillful reading of the tape, but as the result of my analysis of conditions affecting the stock market in general. I wasn’t guessing. I was anticipating the inevitable. It did not call for any courage to sell stocks. I simply could not see anything but lower prices, and I had to act on it….”

General conditions in the US are still strong.

Credit and the broad money supply (MZM plus time deposits) are growing at close to 5%.

Credit risk premiums are rising but are nowhere near alarming. A spread of more than 3.0% between lowest grade investments (Baa) and 10-year Treasuries would flag a warning.

The big shrink, as the Fed unwinds its balance sheet, is still a myth. Banks are drawing down excess reserves at a faster rate, so that liquidity is rising. The rising green line on the chart below shows Fed assets net of excess reserves.

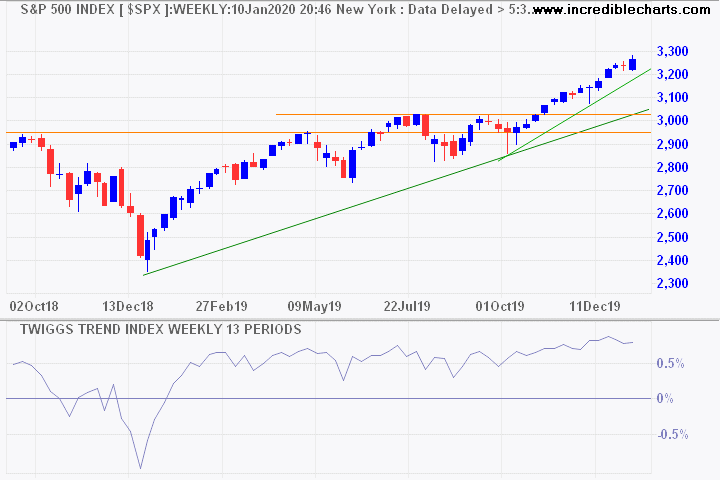

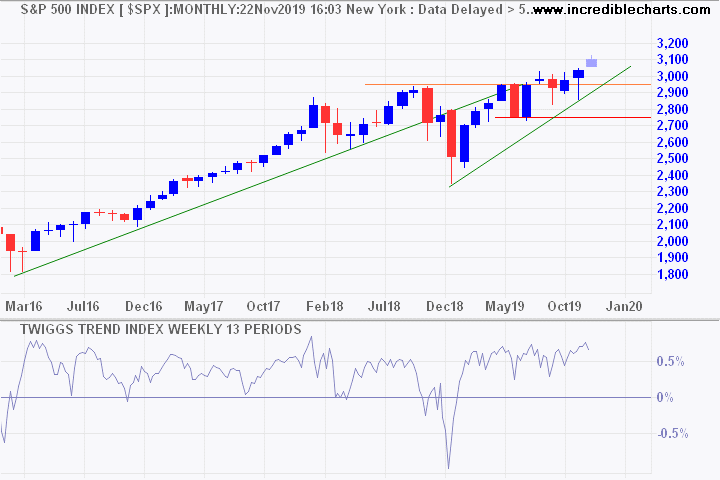

But charts are bearish.

Market volatility is high and a large bearish divergence on S&P 500 Momentum warns of a bear market.

We need to look at global conditions to identify the cause for market concern: Brexit, slowing European growth, but primarily, a potential trade war with China.

It’s time to be cautiously bearish.

There is no training, classroom or otherwise, that can prepare for trading the last third of a move, whether it’s the end of a bull market or the end of a bear market.

~ Paul Tudor Jones