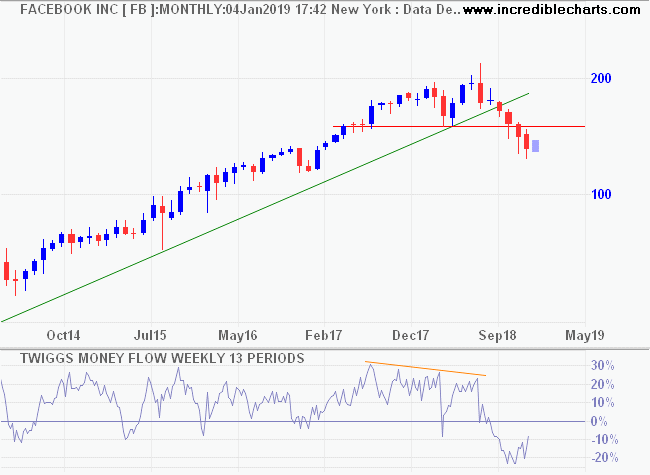

Facebook parent Meta’s shares fell 20% after hours as it said revenue growth will slow, partly because users were spending less time on lucrative services. (WSJ)

Facebook lost about half a million global daily users in the fourth quarter of 2021 compared to the previous quarter, according to the quarterly earnings report of Meta, its parent company. That might not seem like a major drop relative to its under 1.93 billion total daily active users, but it represents a low point for a metrics-driven company whose user base long grew at a rapid pace across its different apps. The statistic shows how Meta has struggled to stay relevant to younger users, many of whom are drawn to competing apps like TikTok. (Vox)

Facebook/Meta’s dissapointing performance is not an isolated problem. Tesla (TSLA), the darling of retail investors — trading at 22 times sales and 93 times forward earnings — is also staring into the abyss. Breaking primary support at 900 last week, TSLA quickly recovered — indicating a false break — but is again testing the 900 support level. Trend Index peaks below zero warn of selling pressure. Breach of support at 900 for a second time would confirm a primary down-trend. Initial target for a decline would be 600 — a 50 per cent fall from its recent peak of 1200.

Jesse Felder shows how precarious the market situation is, with the median price-to-sales ratio at a record 3.5 times. Compare that to the Dotcom bubble, with a peak of just 2.0.

Warren Buffett’s favorite market valuation metric of market-capitalization-to-GDP is not quite as alarming, when you compare to the Dotcom peak in 2000, but nevertheless sounds a grim warning.

We consider MarketCap/GDP to be the most accurate long-term valuation metric available. By focusing on total stock market valuation relative to output, it avoids distortions caused by the financial trickery of stock buybacks and fluctuating profit margins caused by factors like the current supply chain issues.

Conclusion

This is like watching a slow-motion train wreck. The worst I have seen in nearly forty years in financial markets. The Fed may be able to postpone a market crash by several months but the eventual outcome is inevitable. The draw-down has the potential to be truly eye-watering, overshadowing the Dotcom Crash and Global Financial Crisis.

We are overweight Gold (including gold miners), defensive stocks, and key commodities and underweight high-multiple growth stocks.