Good progress has been made combating the pandemic but daily COVID cases seem to be struggling to break through a floor between 50 and 60 thousand. The vaccine roll-out is ahead of schedule but people need to stop listening to idiots like Rand Paul — who went to the Senate gym while infected — and listen to the Chief Medical Adviser whose advice is to wear a mask.

Stocks have paused after the recent run up in Treasury yields. When both stocks and bonds are being sold, there is nowhere to hide.

The Nasdaq 100 is testing support at 12000. At this stage the correction looks mild, with declining Trend Index remaining above zero, but breach of 12000 would signal a test of the Sep 2020 low.

The S&P 500 is performing better but Volatility troughs above 1.0% still warn of elevated risk.

The big five tech stocks are a mixed bag. Alphabet (GOOGL) and Facebook (FB) show strength. Microsft (MSFT) looks stable, while Mazon (AMZN) and Apple (AAPL) are trending lower.

When leaders no longer lead normally signals the final stage of a bull market. The chart below shows the Russell 2000 small caps ETF (IWM) clearly outperforming the large cap Nasdaq (QQQ) and S&P 500 (IVV) indices with all the tech heavyweights.

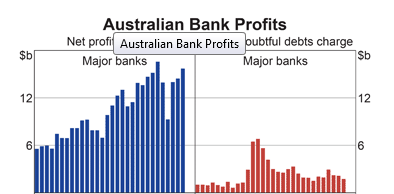

The steeper yield curve benefits banks, who profit from the wider net interest margin. Major banks have climbed 60% to 80% over the past six months, with Goldman Sachs (GS) leading and Bank of America (BAC) the laggard.

Consumer durables sectors are, again, a mixed bag. Household Goods (HG) is flat, Apparel Retail (RA) is climbing steadily, while Automobiles (AU) is down sharply — mainly because of Tesla (TSLA).

Though light vehicle sales were down a million units in February.

And heavy truck sales were down 4,000 units compared to January.

Prospects for the tire industry are improving. Goodyear (GT) retraced to test its new support level after breaking out above its high from late 2019. Respect would confirm another advance.

Conclusion

The recovery is going to be a long hard slog with frequent setbacks. Banks are doing nicely but stocks generally are over-priced and ripe for a major adjustment. There are signs that this is the final stage of the bull market and market risk is elevated.