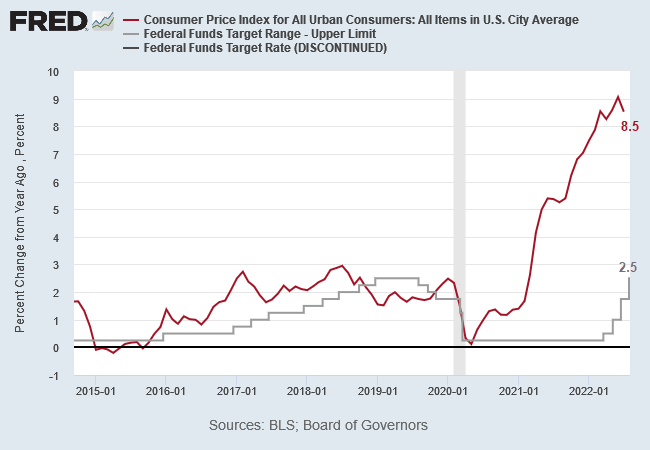

CPI dipped to 8.5% for the 12 months to July. But this still leaves the Fed way behind the curve, with a real Fed funds rate of -6.0% (8.5%-2.5%).

Monthly CPI figures, however, show a sharp slowdown, with CPI falling 0.01% in July (-0.14% annualized rate).

The primary cause is energy prices, which fell 4.53% in July (-54.7% annualized rate).

Food CPI continues to climb, up 1.06%for July (12.75% annualized rate).

CPI Shelter, heavily weighted at 32.1% of the total CPI basket, remains a major source of upward pressure on CPI. The Shelter index tends to lag home prices by up to 12 months and the Case-Shiller 20-City Composite Home Price Index grew at 20.8% for the 12 months to May.

The Rents component of CPI shelter shows a similar lag, a long way behind the Zillow rent index which is up 14.8% over the 12 months to June.

Wages & consumer expectations

Consumer expectations for inflation were unchanged, at 5.3% in June.

While average hourly wage rates moderated slightly, growing 6.2% in the 12 months to July.

Upward pressure on wages is likely to continue for as long as job openings exceed unemployment, with a current shortfall of 5 million workers.

The Fed

The real Fed funds rate (FFR adjusted for CPI) rose to a weak -6.0% after the latest rate hike, still lower than any previous trough in the past sixty years. Real FFR (red below) should be positive when unemployment (blue) is below 5%. Past lows, circled on the chart below, were in response to high unemployment — when the economy had spare capacity. We now have the opposite, with a tight labor market, and negative real rates are likely to give rise to high inflation.

Conclusion

Some are calling this “peak inflation” but the decline in CPI growth is due to a large monthly drop in energy prices. Food and shelter costs are still rising.

The energy crisis is not over, with Winter approaching in Europe while gas storage levels are at record lows and Russia is restricting pipeline flows in an attempt to create division within the European Union. Energy prices are likely to remain volatile.

The Fed is way behind the curve, with a real Fed funds rate of -6.0%. We expect them to continue hiking interest rates despite the recent fall in energy prices.

According to Larry Summers and Olivier Blanchard, the Fed will only be able to bring inflation down when unemployment is well above 5%. The danger is if the Fed is forced to halt rate hikes before it has tamed underlying inflation. We are then likely to end up with both low growth and high inflation.

Our strategy remains defensive: overweight Gold, critical materials, defensive stocks which enjoy strong pricing power, and cash.

Acknowledgements

- Hat tip to Wolf Richter for the CPI Rent/Zillow chart.