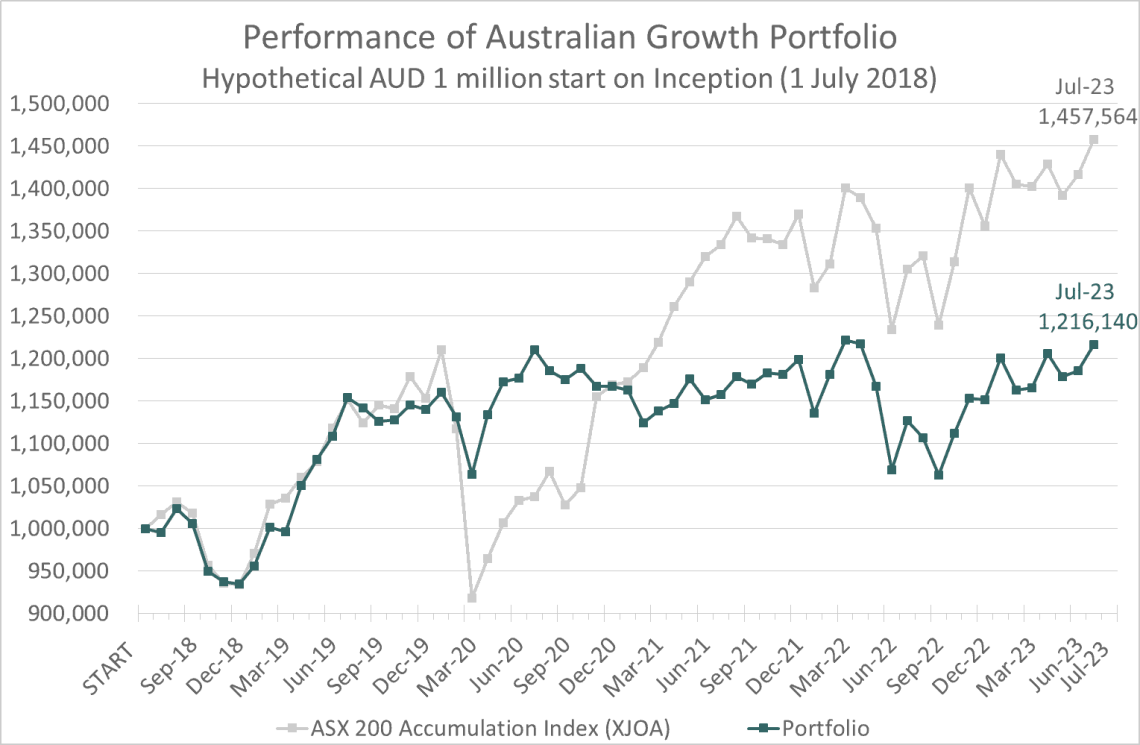

Australian Growth portfolio performance since inception on 1 July 2018 is set out below. We expect to hold most growth stocks for 5 to 10 years.

Individual Stocks

[Content protected for Premium, Australian Growth members only]Past Performance

Hypothetical $1 million invested in the Australian Growth portfolio on 1 July 2018:

Performance Notes:

- Performance is calculated in Australian Dollars.

- Annualized performance is calculated using the CAGR formula.

- Returns are calculated after brokerage costs but excludes all other fees and charges.

- Franking credits are excluded from return calculations.

- Not all stocks have equal weighting nor held for the full period.

- Past performance is not a guarantee of future performance.

Portfolio Allocation

The graph below reflects current portfolio allocation:

For a detailed discussion of target sectors see Changes to Australian portfolio allocation.

Past Allocations

Allocations have evolved over time to deal with elevated market risk, over-priced sectors, and opportunities in cyclicals:

You must be logged in to post a comment.