The Fed is advancing interest rates at a measured pace, with the objective of restoring balance in financial markets rather than to curbing inflationary pressures. Only if inflation spikes is the Fed likely to adopt a restrictive stance.

Elliot Clarke from Westpac sums up the FOMC (Fed Open Market Committee) view from their latest minutes:

Beginning with inflation, whereas the market has recently been concerned that inflation may be getting away from the FOMC (given annual CPI inflation at 2.5%yr and persistent strength in the oil price), the Committee is unperturbed.

Instead of the CPI, the FOMC’s benchmark remains PCE inflation, which is currently 2.0%yr on a headline basis and 1.9%yr for core…..

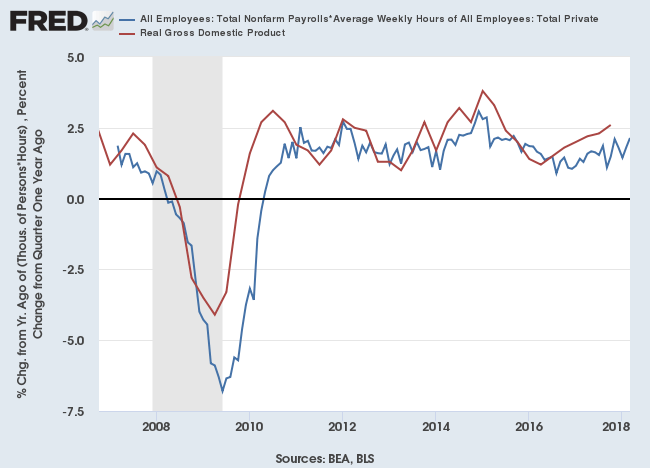

To see upside inflation risks build, a stronger wage inflation pulse is necessary. At present the employment cost index is only reporting “a gradual pickup in wage increases”, and the signal from other wage measures is “less clear”. Two other important considerations for the pass through of wages to activity and thus inflation is that real hourly earnings growth is currently flat and the savings rate near historic lows. The capacity of households to boost consumption and thus inflation is therefore very limited.

Hourly wage rates are growing at a gradual pace.

Personal savings are low.

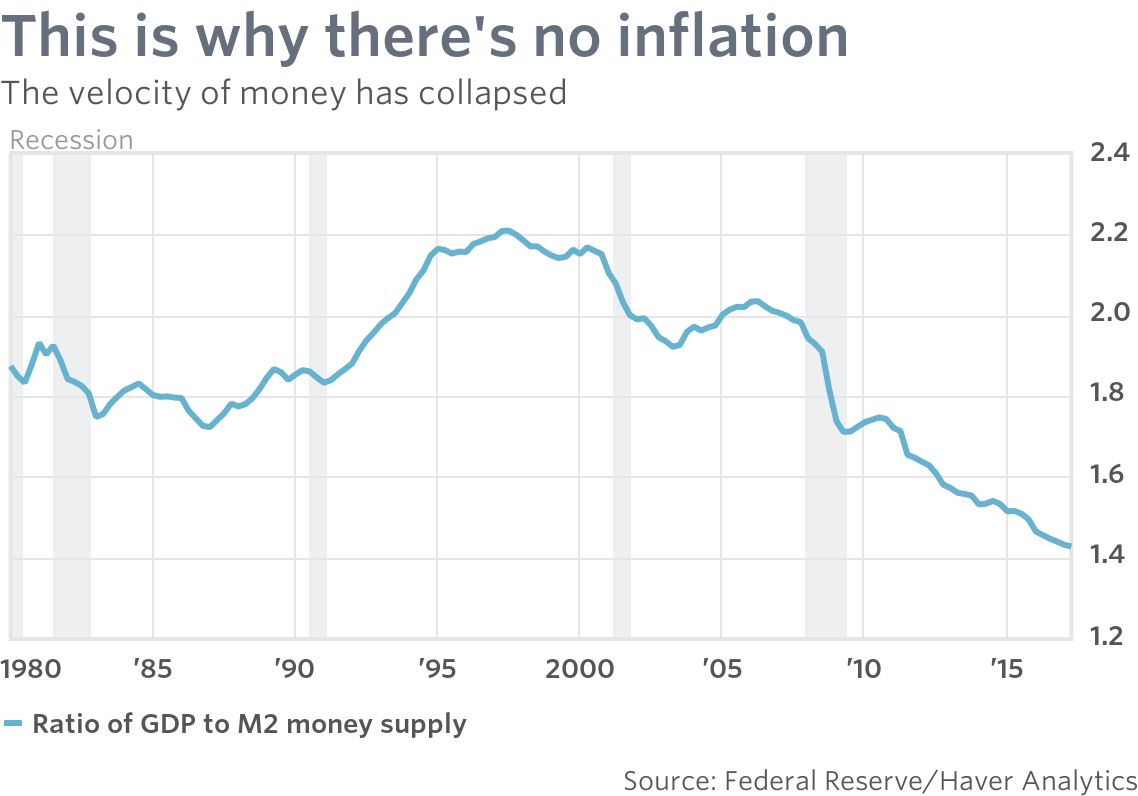

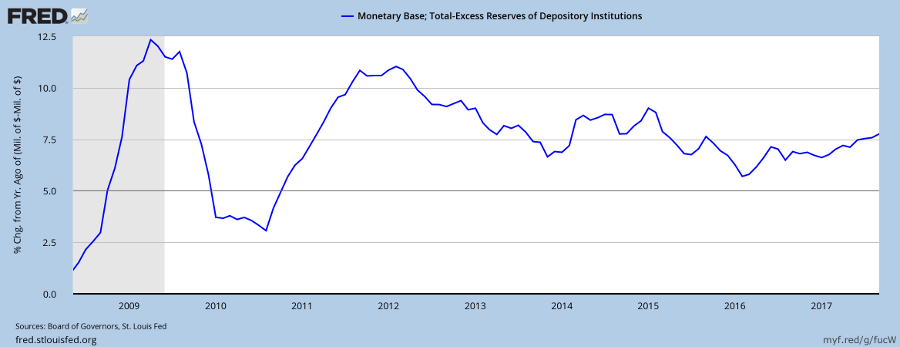

And credit growth is modest.

So not much sign of inflationary pressure.

….Turning to financial conditions, as yet there is no concern of them becoming an impediment to growth or policy. The 10yr yield has moved back to the highs of 2013, but the US dollar has only partly retraced its 2017 depreciation. Further, asset markets remain near recent highs.

Equally significant however is the reference to being nearer neutral and a clear desire to keep the yield curve’s positive slope…..

We do not believe that the yield curve will invert in this instance, in part because higher deficits should see the term premium rise. However, the curve will remain comparatively flat versus history, restricting both the timing and the scale of further rate hikes. This is a key justification for both the market’s and our own view of only two further hikes in 2018 and two more in 2019 – a stark contrast to the FOMC’s seven hikes to end-2020.

A negative yield curve — when 10-year minus 3-month Treasury yields falls below zero — would give a strong recession warning. But the yield curve is only likely to invert if the Fed steps up interest rate increases. With little sign of rising inflationary pressure at present, the prospect seems remote.

You must be logged in to post a comment.